Everyone knows that when interest rates are low, you lock in a long-term mortgage to protect against future rate hikes.

Rates have never been this low and federal government borrowing has never been this high. The government can borrow at 0.28% per year for one to three years. It can even lock-in lending for 30 years at 1.1%—half the normal rate of inflation of 2%. Lending your money to government at interest rates that are half the normal inflation rate guarantees that the money you get back will be worth less than what you lent out. Who would lend so much for so little?

Maybe someone who can print money.

The Bank of Canada has flooded credit markets with $345 billion of newly-created money—almost exactly what the federal government has borrowed since March ($371 billion). The Bank has been buying federal government debt and driving down interest rates to artificial lows.

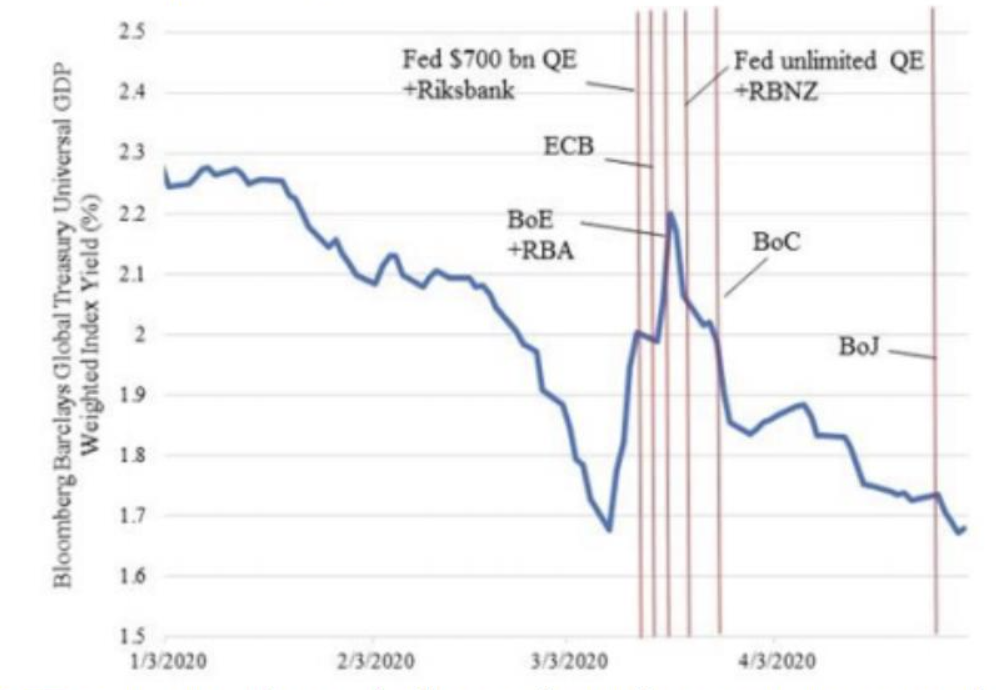

Jon Hartley and Alessandro Rebucci, economic researchers at the Harvard Kennedy School and Johns Hopkins University, produced the below chart showing interest rates on government debt around the world had actually shot up by almost a third from about 1.68% to 2.2% in early March, as the COVID-19 crisis began. But then 19 central banks turned on the printing presses (seen in vertical red lines), making money cheap and rates low.

Bloomberg Barclays Global Treasury Universal GDP Weighted Index (%)

Source: Jon Hartley and Alessandro Rebucci: An Event Study of COVID-19 Central Bank Quantitative Easing in Advanced and Emerging Economies, May 22, 2020.

The graph proves that low rates are not the work of markets, but of central bankers. It would be lovely if central banks could just print money forever—we could have infinite government spending, no taxation and permanently low interest rates—in other words, everything for nothing. Keep dreaming. As former U.S. Council of Economic Advisers Chairman, Herbert Stein wrote: “If something cannot go on forever, it will stop.” The Bank of Canada’s money printing machines will breakdown—or more likely stoke inflation—leading rates back towards normal levels. Even the Bank’s outgoing Governor Stephen Poloz, at the Finance Committee admitted as much: “Yes. When we get back to normal, interest rates will certainly rise.”

Before that happens, you would think the government would lock-in the low rates by securing long-term loans now. I asked Finance officials when they appeared before the commons Finance Committee this week if they had done so. They revealed that of the $371 billion in federal borrowing since the beginning of March, 85% are bonds and treasuries with terms of three years or less. Only 2.4% are locked in for 10 years and a measly 0.7% for 30 years.

So, 85% of this historic new debt is vulnerable to medium-term rate hikes. Finance Department bureaucrats claim they want short-term debt instruments because they are more flexible. Flexible for what? To pay the debt back quicker? You need a sense of humour to believe that this government plans to pay back a penny of this debt. None of the government’s forecasts EVER show it balancing the budget, let alone repaying debt. The debt is here for the long-run even though low-interest rates are not. When rates rise, taxpayers will face sudden and sharp rise in borrowing costs. It will be brutal.

A one-percent increase in the effective interest rate on the government’s $1 trillion debt would cost taxpayers $10 billion/year. Interestingly, a 1% increase in the GST/HST would

raise roughly the same amount. Will the Liberals raise the sales tax by 1% for every 1% increase in debt interest? If not, how else will they get the money?

A more immediate question is why the government is not locking-in low rates for the long run to avoid that eventuality? Is Finance Canada deliberately driving up borrowing costs to please bondholders who collect the interest? Have the bankers duped government? Whatever the answer, it is clear that just as government spends stupidly, it borrows stupidly.

There are two important lessons:

First, the rich win big when government goes deep into debt. Government debt is owed to people rich enough to lend it in the first place. These wealthy folks collect all the interest on it. That represents a wealth transfer from working class taxpayers to wealthy bondholders.

Second, Canada may face a massive financial crisis when interest rates rise. Household debt will rise to 200% of disposable income by the end of this fiscal year, shattering all previous records. Before the coronavirus crisis, households were already spending a record 15% of their income on servicing their debts. That is with rates at all-time lows. Corporate debt is piling up and governments at all levels will add over $300 billion in new debt this year. Combined household, business and government debt will be about four times the size of our entire economy by the end of 2020.

We have never attained anything like these debt levels in the post-war period, including in the 1990s when the debt-drunk federal government had to stop borrowing because literally no one in the world would lend to it. At that time our total public and private debt was only 256%, barely half of what we have now.

What do we do about it?

First, the government must begin selling long-term bonds on any debt that comes up for renewal, to lock-in low rates for 30 years or more. Second, COVID-19 spending must be allowed to lapse on schedule. These programs cannot go on forever. Third, the government must immediately approve $20 billion of natural resource projects up for federal environmental approval and signal to the market that others will get prompt approval as well. We cannot afford to leave trillions of dollars of resource wealth buried beneath the dirt while we go bankrupt. Fourth, federal spending growth must come under a strict cap, so that the economy can catch up with the cost of government and the debt-to-GDP can begin downward.

The alternative is that we keep borrowing staggering sums at variable rates until interest rates rise and households, businesses and governments collapse under the weight.