Bill Morneau has told Parliament 20 times that the government’s “balance sheet” is strong.

On May 13th, I asked the Finance Minister to tell us about the balance sheet’s three main parts: assets, liabilities and equity.

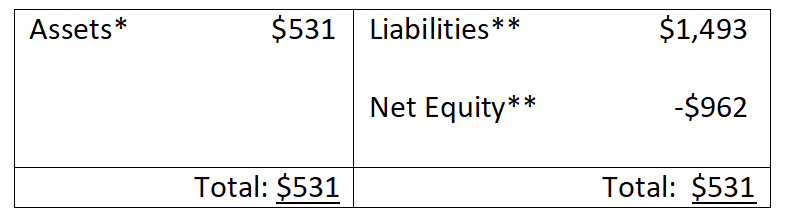

What is the dollar value of the assets on the government’s balance sheet?

No answer.

How about liabilities?

No answer.

Equity?

No luck.

If he does not know any of the three balance sheet components, how could he possibly say the balance sheet is strong? In truth, the government doesn’t actually publish anything called a “balance sheet”, contrary to the Finance Minister’s constant use of the term. (Throwing around words with no thought to their meaning can be a dangerous thing). The government does publish a “Consolidated Statement of Financial Position” (which is now more than a year out of date) and a “Condensed statement of assets and liabilities”, but nothing called a “balance sheet”.

But pulling from reports by Finance Canada and the Parliamentary Budget Officer, we can extrapolate one.

Estimated for End of 2020/21 (in billions)

Sources for table:

* Finance Canada Fiscal Monitor: February 2020.

**Parliamentary Budget Office: “Scenario Analysis Update: COVID-19 Pandemic and Oil Price Shocks”.

(Liabilities extrapolated from PBO’s estimate of March 31, 2021 federal debt).

The “net equity” is often called the “federal debt”, which is a deceptive term. Normal people would say that the debt is the total liabilities of $1.49 trillion. What government calls its debt is actually the net worth… which is negative $962 billion. You read that correctly: if the Government of Canada sold all its assets and put all the proceeds into paying debts, it would be left with a negative net worth of $962 billion—almost a trillion dollars.

Lop off some zeroes to make the numbers more digestible. Imagine your only asset was a $531,000 house and it had a $1,493,000 mortgage—a mortgage three times the value of the house. Your net worth would be minus $962,000. You would give the keys to the bank and walk away from your house bankrupt.

So, why is government not yet bankrupt? Because its balance sheet has an invisible asset whose value is literally priceless: taxing power. The asset is the net present value of all future taxes government can collect. It is the only reason governments can defy financial gravity and avoid collapsing under crushing debt.

Can the federal government really count on taxpayers to prop up its trillion dollars of negative net worth? Advocates of deficit spending say “yes” because the federal government’s debt-to-GDP ratio will only be about 50% at the end of this fiscal year, below the 66.6% in the mid-1990s when the Wall Street Journal called Canada “an honorary member of the Third World,” and the lending markets literally refused to lend the government another cent.

It’s true that Canada’s debt is not as bad as it was in the mid-1990s. It’s worse.

Yes, the federal debt-to-GDP is lower now. But the total debts of all levels of government, businesses and households are much higher. There is no point drawing a distinction between public and private debt. They are all intertwined and supported by the same economy. The invisible asset on the government’s balance sheet—taxation power—becomes much less valuable when heavily-indebted businesses and households cannot afford taxes. Conversely, household and corporate debts become the debt of government, which must bailout families and firms in a crisis, as we now see. For example, the government-backed Canadian Mortgage and Housing Corporation (CMHC) now insures a half-a-trillion dollars of mortgages. When households default, government picks up the tab and vice versa. So, the only thing that matters is the total public and private debt as a share of GDP.

The economy is like a horse carrying big bags of debt on his back up a hill. There is just one horse who must carry not only federal government debt, but also all the provincial, municipal, household and corporate debt. As of 2018 (BEFORE COVID-19!), total public and private debt equalled about 356% of GDP. So, the horse carried more than three and a half times his weight that year.

Worse, the horse is now starving while his owners are piling hundreds of billions in new debt on his back. Household debt as a share of GDP will rise from today’s record 100% to 130% by the third quarter of this year, says the CMHC. Businesses are also adding massive debts just to stay

alive during shutdown. All told, total private and public debt could reach 400% of GDP by the end of this fiscal year. These numbers would crush previous records, and are far higher than the 275% we had in the debt crisis of the mid-1990s.

The only difference now is interest rates are lower. When they rise (and they will), these debts will break the horse’s back. Whispering in his ear about imaginary “balance sheets” will not stop him from collapsing. He is a horse after all. Not a unicorn.